The office market is sexy. Big buildings, glistening skylines, and trillions of dollars of value are all reasons why there is so much attention and headlines surrounding the office market.

But the office markets are hurting. And this is not a normal cycle. Here’s how companies with offices can make the most of it…

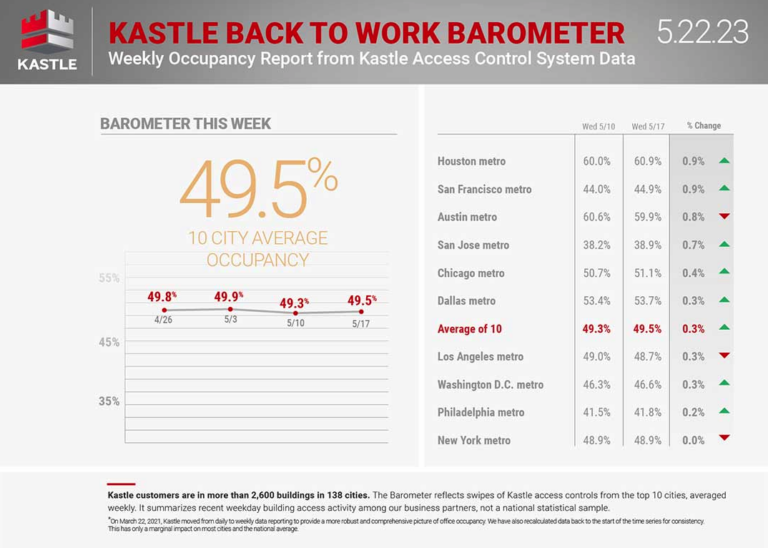

One of the most alarming and over-publicized statistics came from Kastle’s “Back to Work Barometer.”

According to Kastle, that 60-story office building you see on the horizon is only 49.5% occupied. Its peer in Dallas? Only 53.7% occupied. New York? 48.9%. Yes…less than 50% occupied.

Stunning, right? And what is troubling is that it appears to have stabilized at less than 50% occupied. According to an article in this week’s WSJ, the pace of the return work has stalled, vacancies have risen, and rental rates are starting to sink.

I’m not sure Kastle has it right. But I have heard a lot of “happy talk” from bullish landlords and Pollyanna City leaders, and I do not believe they have it right, either. There’s a storm brewing in Uptown.

Because even if Kastle is off by 50%…why would anyone build an office building in this market?

Other than red-hot Miami and super cool Austin, Charlotte’ South End is the only place where new class-A speculative office towers are being built in the US.

You can see it for yourself: towers are being built in South End while six buildings in Uptown are on the watchlist for foreclosure…only a mile and a half away.

(Is your building on the foreclosure watchlist? Email me to get the list.)

South End is creating an interesting dynamic for Charlotte. Like the chamber with the golden idol that attracts Indiana Jones, South End is luring a new workforce and a new demographic…and there are hidden traps for Charlotte in this development that you may not be aware of.

Why is South End growing while nearby Uptown shrinks?

Three things jump out at me…

The first one is Gen Z. According to the US Census Bureau and a study by The Charlotte Alliance, around 80 people are moving to Charlotte every day, and more than half of those have a college degree, and the median age is 30.7.

My son, Mac, is one of them. He graduated last weekend from Miami (Ohio), and he doesn’t want to move to Charlotte; he wants to move to South End. That’s all he and his friends talk about.

Mac says he is ready to “get on with it.” He wants to go to an office, meet new friends, and be independent. His friends tell me much of the same thing.

For young graduates at a time in their lives when everything seems uncertain, South End is like a giant beacon where jobs are plentiful, and the beat goes on and on.

Here’s the second reason South End is exploding while Uptown is quiet:

The would-be employers of these fine graduates are still wrestling with how to get employees back into the office.

Uptown employees who left kicking and screaming are now fighting not to return. They feel more efficient working remotely from South End and resist the idea of battling traffic to return to what they feel is a staid work environment in Uptown.

The start of 2023 saw over 50% office occupancy rates for the first time since before the pandemic. But recently, the return-to-office rate has stagnated. According to Scoop Technologies, 58% of companies allow employees to work part-time from home, with companies requiring full-time office presence declining to 42%. These trends are mostly driven by employee preferences—saving on office costs seems to be a smaller factor.

Here’s the third reason why South End is growing at Uptown’s detriment….

Another big challenge to getting people back in the office is “flex schedules.”

People are arriving late or leaving early to avoid traffic. This means they are not going to lunch or staying after work for a drink or dinner with comrades. The result? Dark storefronts and no buzz in Uptown.

“The highest paid attorneys in our office only want to come to work on Wednesday because that is free-lunch day.”

—an Uptown law firm manager.

The tail is wagging the dog.

And that’s a big problem because, for many companies, rent is the second-largest investment—outside of personnel.

Where an employee can be gone in thirty days, and a short-term lease is seven years long…most of them are fifteen years and longer; office managers have a huge burden, and it’s a mess.

And more and more, we are seeing that real estate decisions are getting messy, usually because they’ve been delegated to lower-level managers who have no clear mandate.

After all, no one has ever gotten a promotion because they made a great decision on office space—people have been fired because they made a bad decision on a long-term commitment to a landlord.

So what’s the solution here for companies?

It’s not hiring a traditional corporate broker.

During the consultation phase, our competition will be half-heartedly doing work for you on the front end.

And the minute they start realizing that there’s no deal to be made, or if there’s information that they know will influence your decision to either take less office space or not make a move at all, they might think twice about sharing it with you. They’ve got all this time invested in the deal; they’ve got to transact. For them, it’s not about what’s in your best interest.

Instead, we suggest using The Strategic Tenant Advocate™. It’s a process we’ve created that leads to flexibility for tenants, confidence in the budget, no surprises, and extreme advocacy.

If you’re interested, we’ll walk you through it.

We’ll also work with you to help you make the best decision for your business and your space.

And unlike other brokers, we’ll reimburse you for any consulting time if our collaboration results in a transaction.

Think it’s worth learning how we can help you navigate this difficult time for office spaces?

Email or call. We’re standing by to help.